Weekly Markets #3

Market recap for April 4th 2026

The current playbook is getting slightly boring at this point: ceasefire rumor sends everything ripping, Trump escalates, rally dies. Tuesday’s 2.9% surge on reports Iran was open to ending hostilities was the best session since May. Then Trump’s Wednesday night address promised to hit Iran “extremely hard” for weeks. The S&P round-tripped 250 points in 48 hours.

The real surprise came after Friday’s close: March payrolls at +178K, crushing the 60K consensus and reversing February’s ugly -133K revision. Unemployment dipped to 4.3%, wage growth cooled to 3.5% year-over-year (lowest since May 2021). That combo, strong hiring with cooling wages, is exactly what the Fed needs to stay put. It takes the recession panic down a notch.

Monday’s open, also happens to be Trump’s April 6 Iran deadline. That double catalyst creates decent gap risk setup.

The macro picture stays stagflationary. Oil above $110 with the Strait of Hormuz still effectively closed is a growth tax no central bank can offset. The IMF warned the Fed has little room to cut. Futures now price a 77.5% chance of no move through year-end. Private credit cracks showed up too, with Apollo and Blue Owl gating funds at steep discounts.

On the other end of the spectrum: SpaceX filed for what would be the largest IPO in history at $1.75 trillion. Buffett says stocks still aren’t cheap enough. Credit spreads actually tightened on the week, which is the one signal arguing this correction stays orderly.

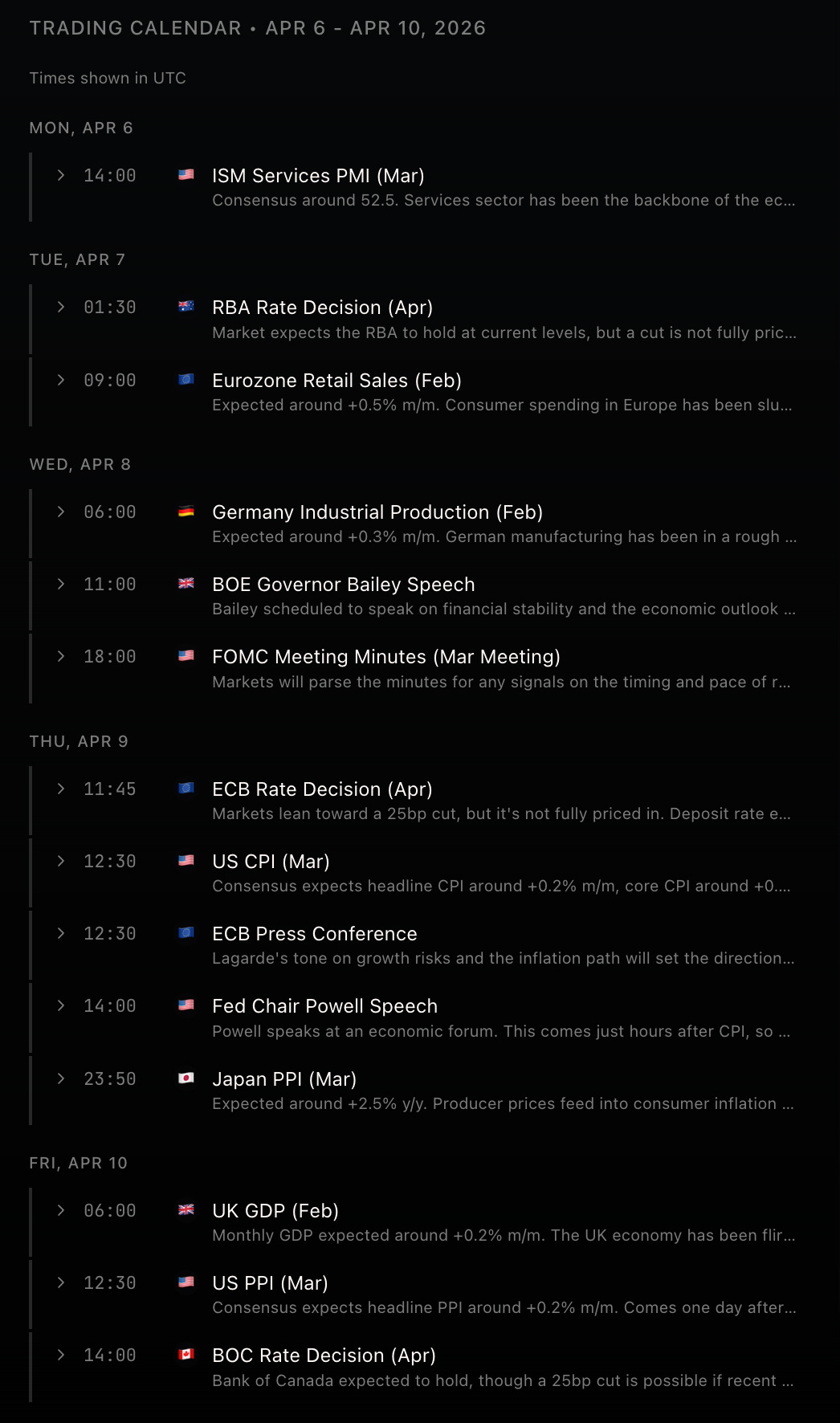

For the upcoming week, Wednesday is the day. US CPI drops in the morning, Powell speaks hours later, and the ECB delivers its rate decision right in between. Hot core CPI with a hawkish Powell reprices rates, equities, and the dollar for the rest of April. A soft print with a dovish lean rips risk assets and probably sends the 2-year through recent support.

The setup heading in: the US economy is still running warm while the rest of the world looks fragile. Europe is stuck in low gear. German industrial production is in the gutter, Eurozone retail barely growing. The ECB will almost certainly cut 25bps, but the real question is what Lagarde says about the path forward. A pause signal bids the euro. A growth scare keeps front-end European yields falling.

Outside Wednesday, the calendar stays packed. Monday’s ISM Services PMI sets the tone for US growth expectations. The RBA overnight Tuesday is a coin-flip that will whip AUD. Thursday brings UK GDP, US PPI (feeds directly into the PCE estimate), and a Bank of Canada decision where a surprise cut isn’t off the table.

All Quiet on the Western Front.

Side note before diving into this week's market review: if you want analytics for over 1000 markets across options, crypto, and futures while learning systematic trading strategies that harvest different risk premiums across multiple asset classes, check out tradingriot.com. Use code “ANALYTICS” for 50% off your first month.

S&P 500 & Equities

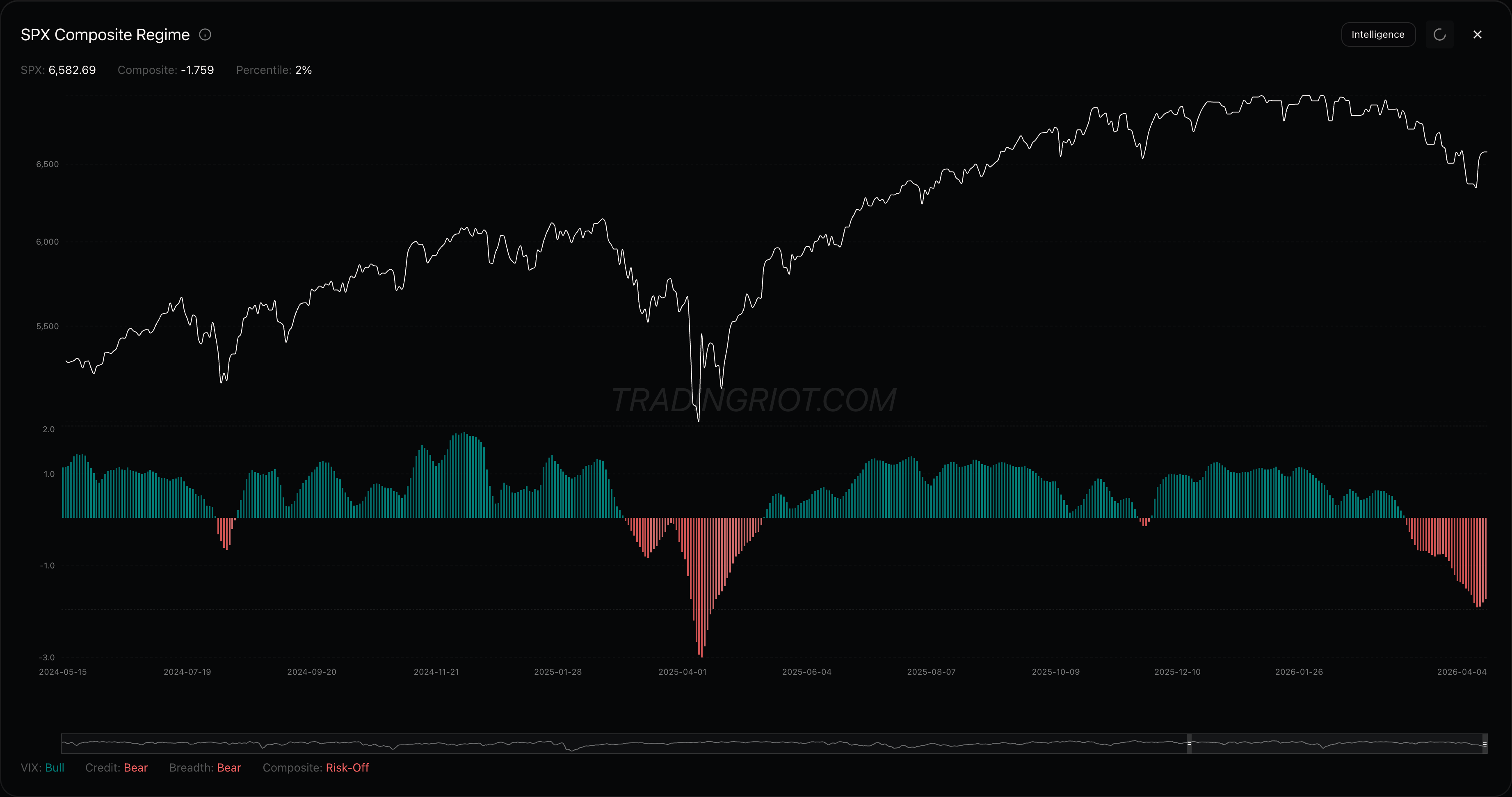

SPX closed at 6,583, up 1.6% on the week and snapping a five-week losing streak. The path was definitely ugly to say at least.

Composite regime still sitting heavily in negative, while this move down still lacking the panic leg down which is a classic SPX signature.

Chart is sitting at prior support acting as resistance now, first sign of possible relief is the fact momentum oscillator flipped positive, but I would still prefer to wait for price reclaiming key levels before calling the bottom.

Mega-caps led the bounce. Meta gained 9.3% on the week, clawing back some of its 14% monthly drawdown. GOOGL ripped 7.7%, NVDA bounced 5.9%, AMZN 5.1%, MSFT 4.5%. The NVDA and AMZN moves look like textbook short-cover rallies off deeply oversold conditions. NVDA is still sitting 21% below its all-time high, firmly in bear market territory

Tesla was the laggard, down 0.5% after Q1 deliveries missed at 358K versus 365K consensus, a 14% sequential drop from Q4. Nike cratered over 10% early in the week after guiding China sales down 20% annualized, a canary for the consumer discretionary complex under $4/gallon gas.

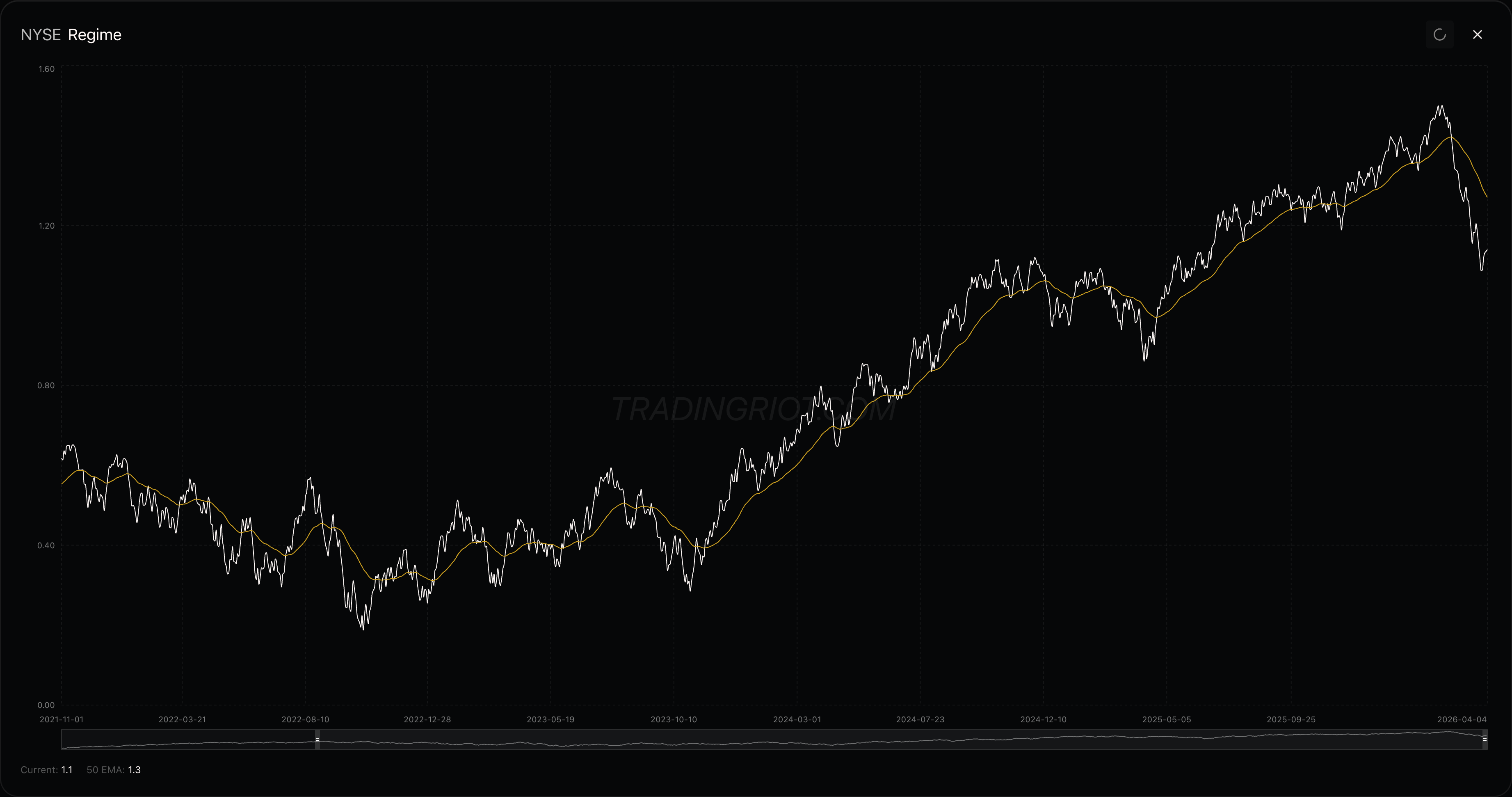

While breadth had slight relief this week, we are still in deep bear territory.

Sectors

Don’t let the headline number fool you. Every single sector outside energy carries a negative one-month return. The bounce was narrow. Tech (XLK +3.3%), financials (XLF +3.6%), and consumer discretionary (XLY +2.4%) all participated, but the defensive bid underneath is still intact: XLP was basically flat on the week with 17.6% IV, the lowest of any sector by a wide margin.

The most telling signal: XLE dropped 5.3% despite oil surging 12%. That’s the market pricing demand destruction over supply premium. When energy stocks fall while crude rips, the macro message is bearish.

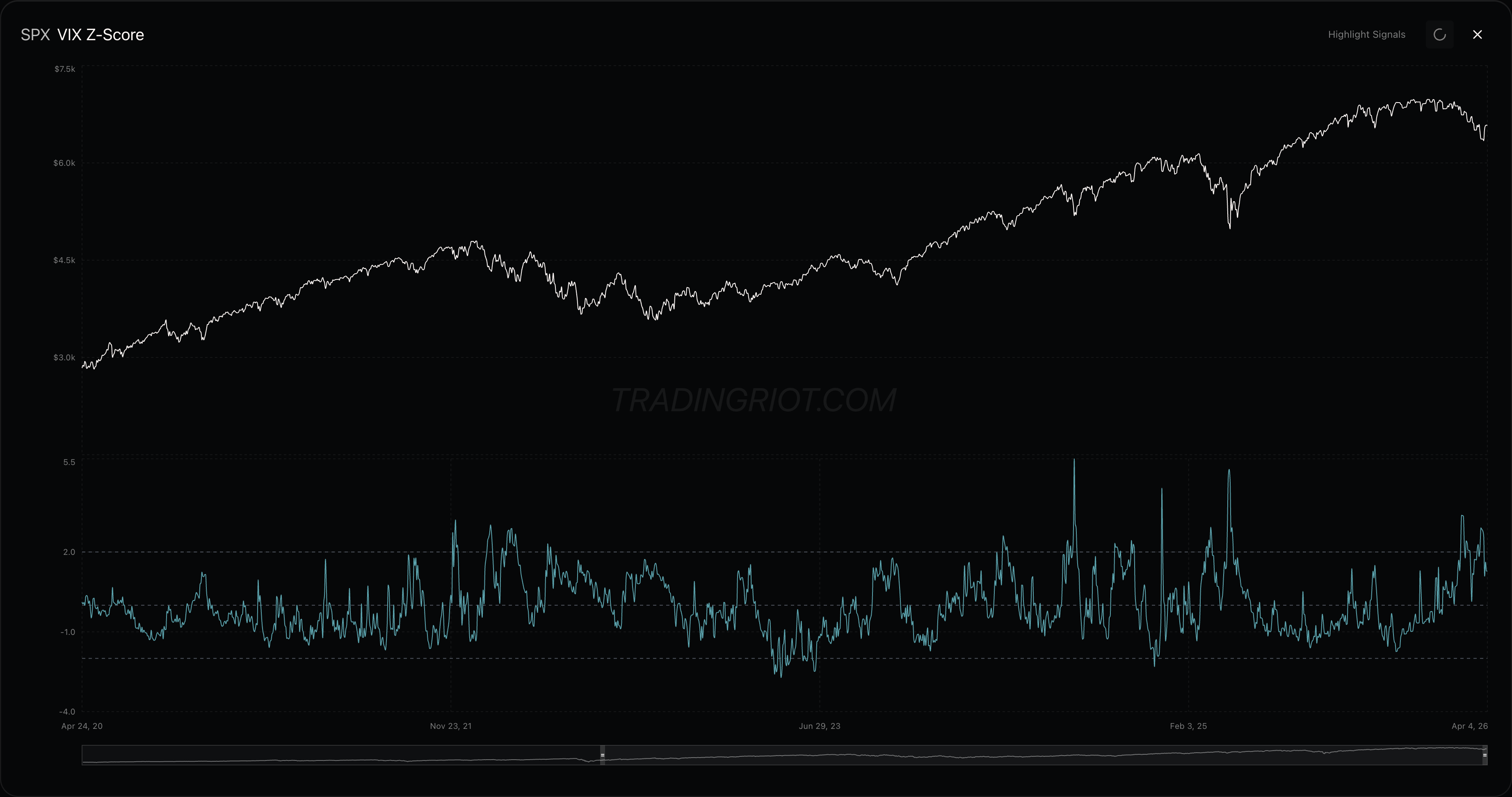

VIX

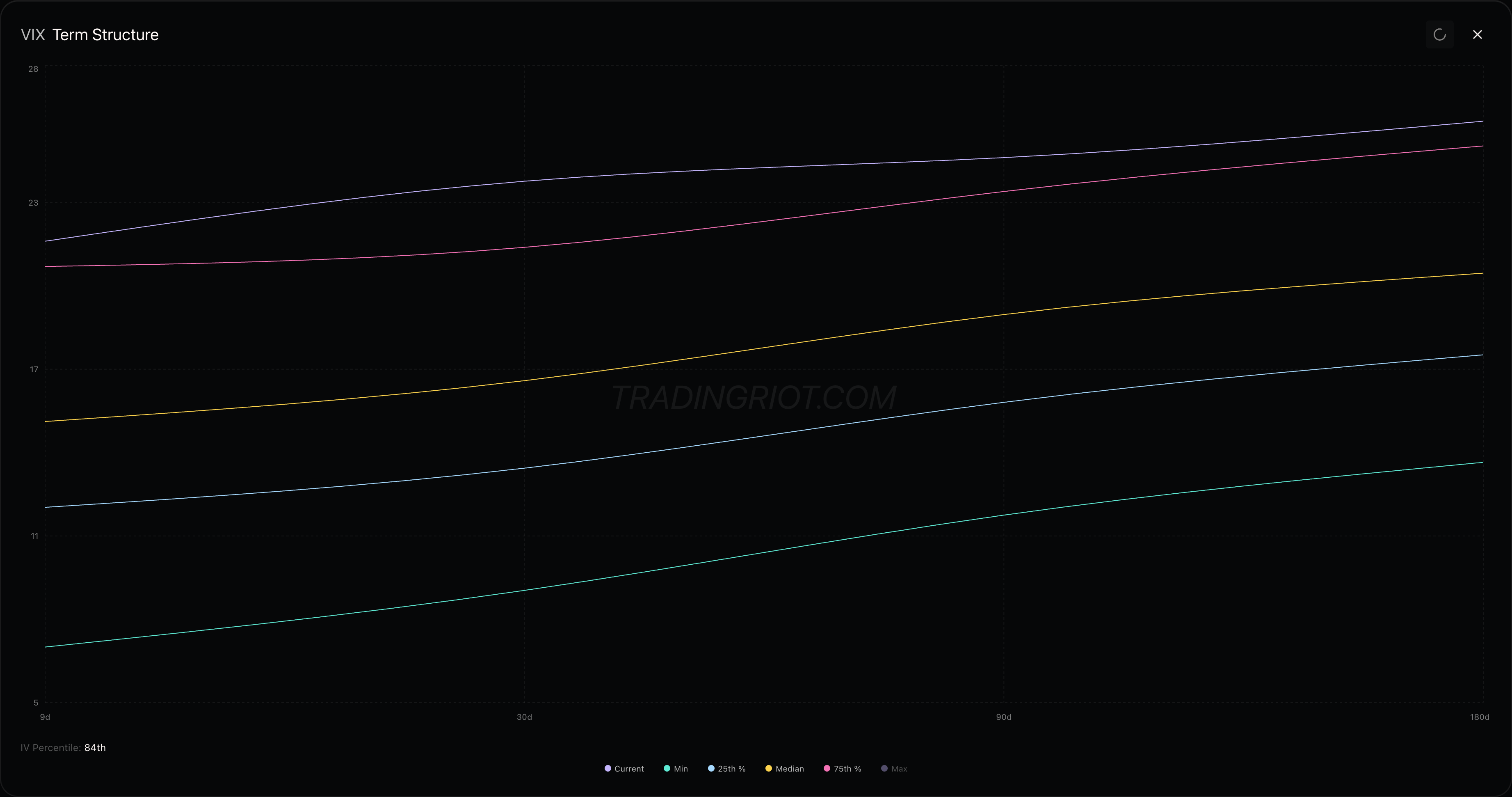

VIX collapsed from 31 to 23.9 on the week, a 13% decline, but the intraday range Thursday (21.7 to 27.9) tells you nobody is comfortable with their positioning. The term structure flipped from deep backwardation Monday to mild contango by Thursday’s close, but VIX6M above 26 says the market expects this volatility regime to persist well into summer. Anyone running short gamma was definitely sweating this week.

The overall VIX z-score is still elevated, hovering around 2. This is a very hard environment to trade VIX, as the market is missing that classic elevator-down move. Instead, VIX is just having a huge back and forth intra-week.

Credit Spreads

Credit actually improved. HY OAS compressed from 346bp to 316bp, IG from 93bp to 87bp. That’s the one signal arguing this correction stays orderly rather than turning systemic. Bond traders are treating the selloff as headline-driven, not fundamentally deteriorating. VIX at the 84th percentile with a flat term structure and credit tightening is signaling elevated uncertainty, but not panic.

Overall I think think that while markets bounced this week, I am personally not very eager to start buying the dip yet as everything is looking far from panic.

Crypto

While there were some nice intraday rotations in Bitcoin and altcoins, from a higher timeframe point of view prices stayed more or less flat this week, favouring short vol strategies for those brave enough to sell Bitcoin vol amid the Iran conflict.

On the regulatory front, the SEC and CFTC jointly classified 16 cryptocurrencies as commodities, which is structurally positive for product development and institutional access. Coinbase also received OCC trust charter approval, adding another institutional rail. On the other side, Strategy paused BTC purchases for the first time in 13 weeks, sitting on 762,099 coins at a $66,384 average cost, essentially breakeven.

Besides the two narratives in HYPE and TAO which were covered in previous posts and also slightly lost strength by now, there doesn’t seem to be much appetite for taking risk in crypto, which makes sense.

For Bitcoin, April closed as an inside month where the monthly highs and lows should bring a reaction when tested, although I’d still be surprised to see price revisiting the yearly lows.

Rest of the market

Crude oil was the week's dominant force, surging 11.9% to $111.54 with the Strait of Hormuz still at 96% reduced transits and Lloyd's refusing to insure passage. The commercial index on crude sits at 100, the maximum bullish reading from COT data, meaning commercial hedgers are positioned for sustained high prices.

Gold continued its run, up 3.6% to $4,652 with a 95.2 commercial index. The safe-haven narrative has some cracks though, as a handful of central banks have been forced to sell gold to fund wars, defend currencies, or cover energy costs. The aggregate picture is still net buying, but if oil stays elevated and more nations get squeezed, forced selling could pick up.

Last week I flagged the heavy put skew in gold and the opportunity in selling those puts. That turned out to be the right call as price rallied through the week. Silver followed, up 4.6% to $72.74 with a 98.4 commercial index.

The dollar index was flat on the week but the broader trend remains up. Large speculators are long dollar futures, which normally flags a crowded trade, but reserve currency flows, the rate differential with a cutting ECB, and the fact that $110 oil means the entire world needs more dollars to buy energy keep overriding that signal. As long as 99 to 98.5 holds on DXY, I expect dollar strength to persist.